Intel in Oz

What to make of Intel's turbulent few weeks?

A little more than a year ago I wrote Intel’s Immiseration …

I included a quote from, then Intel CEO, Pat Gelsinger:

I have no illusions that the path in front of us will be easy. You shouldn’t either. This is a tough day for all of us and there will be more tough days ahead.

While Pat was correct, the tough days for him at Intel ended with his departure on 1 Dec 2024. His replacement Lip-Bu Tan, however, has already seen plenty of such days in the few months that he’s been in charge.

That post closed with a question:

And it’s left a, still unanswered, question. Intel couldn't break into smartphone SoCs with clear process leadership and the financial strength to invest heavily. Why should it be able to break into other competitive markets today when it no longer has those advantages?

Twelve months on that remains the key question. More specifically Intel needs lots of cash (maybe up to $50 billion) and it needs customers, and at least one big one, for Intel Foundry, and it needs them soon. Where will they come from?

My first draft of this post was titled ‘Intel’s Humiliation’ (rhymes with ‘Immiseration’). The bones of the company are being picked over very publicly, including in the leading article of this week’s Economist:

The front cover of the newspaper doesn’t mention Intel but the firm is the ‘spectre at the feast’ in the cover illustration.

The article itself says, in a less than ringing endorsement of the firm:

Either way, the federal government should not throw good money after bad. Taking a stake in Intel would only complicate matters.

It was certainly personally humiliating for Lip-Bu Tan to be called on to resign by Donald Trump, and to be summoned to meet the President at short notice.

Yet, out of that humiliation came a glimmer of hope.

Lip-Bu Tan emerged from the Oval Office with his job intact and more: the Trump administration would take a 10% stake in Intel.

Yesterday, though, it became clear that ‘take’ really did mean take (as in shoplift).

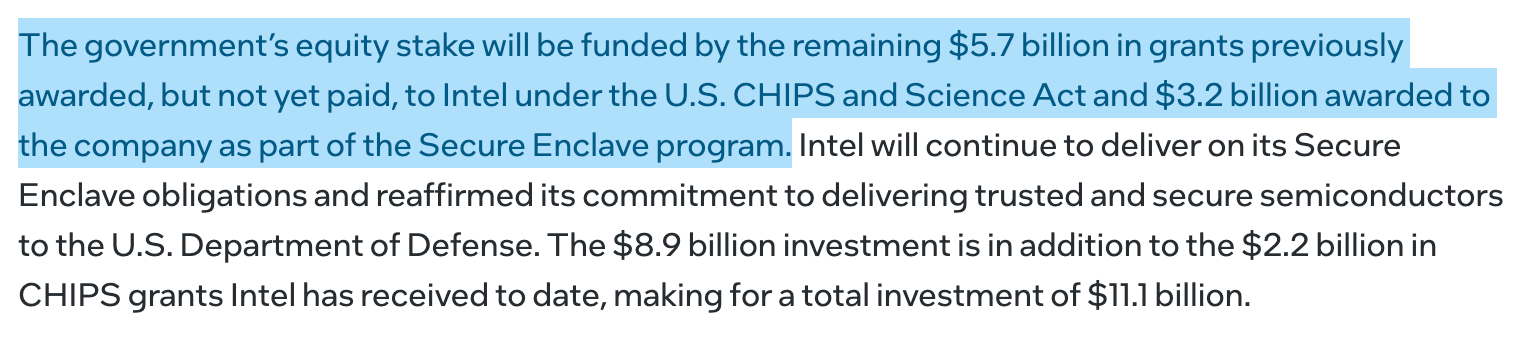

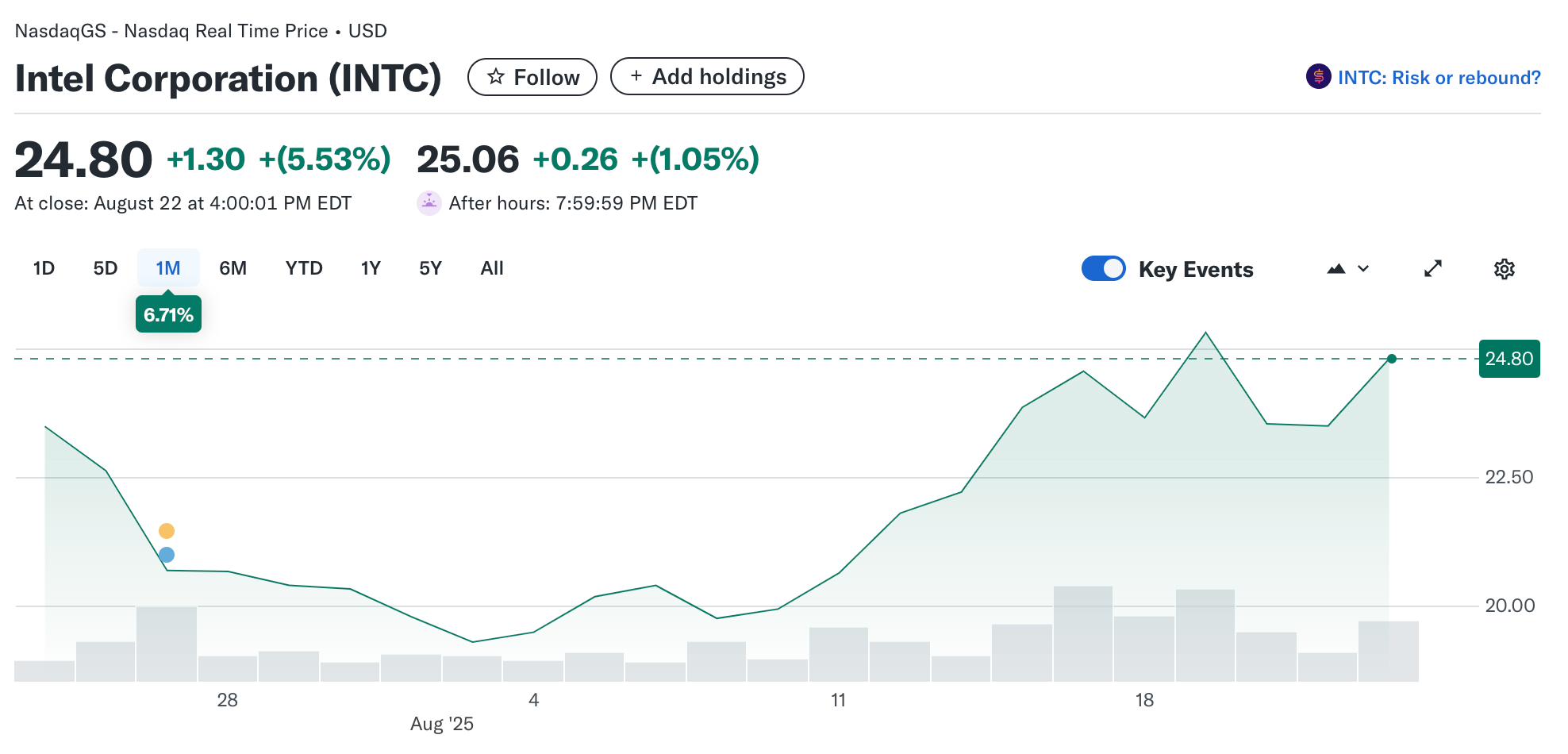

The $8.9 billion isn’t new money but the conversion of previously awarded grants into equity. This must be awful for Intel shareholders? Strangely the stock rose on the news from the Oval office, even rising a little when the nature of the investment became clear.

The reason for this? Well one explanation is that the government now has ‘skin in the game’ on a personal level. Trump and Howard Luttnick’s reputations (as far as they go) rest on ‘the art of the deal’. This ‘deal’ was a ‘steal’ but they won’t want it to go to zero.

Ben Thompson makes a clear case for why ‘skin in the game’ is important:

The single most important reason for the U.S. to own part of Intel, however, is the implicit promise that Intel Foundry is not going anywhere. There simply isn’t a credible way to make that promise without having skin in the game, and that is now the case.

And the administration has the tools, should it choose to use them, to help Intel. If it was willing to slap 15% tariffs on Nvidia and AMD GPUs being sold to China, then it can certainly lean on these firms, and others, to become Intel Foundry customers. Maybe also to persuade those firms to stump up some of the cash Intel needs in advance: let’s face it Nvidia, at least, can afford it.

For an example of just how things are working at the moment here are some Trump comments on Nvidia:

Reporter: Two questions, one about China... Your administration agreed to send the most advanced Nvidia and AMD chips to China.

Trump: Obsolete chips. No, this is an old chip that China already has. I deal with Jensen, great guy from Nvidia. It's an old chip. China has it in different form or combination. He has a new chip, the Blackwell—super advanced. I wouldn't approve that. But for H20, I said I want 20% for our country. He said make it 15%. We negotiated a deal. On Blackwell, he's coming to see me about an unenhanced version.

And then here is Trump on the Intel stake:

Treasury Secretary Scott Bessent was quick to dismiss the idea of pushing firms to use Intel, but Bessent is just one voice in the administration and in any event policies change from week to week, or even from day to day.

Here’s

making the case for doing this ‘bullying’:It’s time to invest in the American (gold-plated) foundry of the future. I believe that large foundry partnerships will be announced as part of ongoing investments in America. In theory, Foundry needs orders to exist, and this is how they will get them.

Trump can bully Broadcom, Nvidia, Qualcomm, Apple, and AMD to put orders towards Intel, while possibly forcing Amazon, Microsoft, Google, and others to make a large investment in the fab itself (or push orders). Additionally, forcing semicap companies like KLAC, Applied Materials, and Lam Research to invest and give resources in exchange for approved licenses is another example of a carrot and a stick. I think Trump could forge the giant partnership to happen, but then execution is all up to Intel. And LBT is still once again qualified for the job.

Doug’s post is, as always, well worth reading in full:

And here is

suggesting that Intel should act as a ‘second source’ for Nvidia.Of course, this is all more than a little dubious. The Washington Post explains why it thinks this equity investment is a terrible idea:

President Donald Trump’s announcement on Friday that the U.S. government will take a 10 percent stake in long-struggling Intel marks a dangerous turn in American industrial policy. Decades of market-oriented principles have been abandoned in favor of unprecedented government ownership of private enterprise. Sold as a pragmatic and fiscally responsible way to shore up national security, the $8.9 billion equity investment marks a troubling departure from the economic policies that made America prosperous and the world’s undisputed technological leader.

I think that this is a bit overdone. TSMC was founded with the Taiwan government owning a large stake. Governments have owned or own stakes in a range of other semiconductor firms including STMicroelectronics, SKHynix, and Renesas, to say nothing of the Chinese governments stakes in various firms. The US Government had stakes (through warrants) in carmakers and airlines following the financial crisis. Like those firms, Intel is now seen as a vital piece of infrastructure.

But the Washington Post take ignores the elephant in the room. Does anyone think that leaning on Intel to increase that 10% shareholding to 15% or more is out of the question?

We’re left with a lot more questions than answers.

Will the administration deliver customers to Intel? Who knows?

Will it persuade other firms to provide Intel with the cash it needs? Again who knows? (I think it unlikely, however, that the administration will provide any more cash itself).

Will all this save Intel Foundry? Again, who knows?

Is this a sensible approach to the management of a key strategic asset? Probably not!

And, perhaps most fundamentally, is this amenable to careful and rational financial and technical analysis? Almost certainly not! (I don’t blame anyone for trying though).

Does any of this make much sense? No! This newsletter tries to learn from history. Sometimes, though, you have to throw the history away and admit that it’s of little value. Now is one of those times. It’s now Calvinball. The rules have changed, or perhaps it would be more accurate to say that there are few rules.

In the Wizard of Oz, Dorothy suddenly realises that she’s not in Kansas any more.

Here’s the thing, though. Intel’s manufacturing business was on a seemingly inevitable and accelerating path to oblivion. The Trump administration, like the storm in the film, has picked it up.

Who knows where it will land? Maybe it will be torn to pieces. Maybe, just maybe, though it will be taken on a spectacular journey, and Lip-Bu Tan and his firm will land in a much better place.

I can’t promise any answers, but after the break, some more thoughts for paying supporters on Intel’s predicament including on breaking the firm up, the claims of ‘passive ownership’ and more on that Economist cover.